The Law to Develop Production, Attract Investments, Generate Employment, Fiscal Stability and Balance (“Law of Productive Development”) was published in the Official Registry and is consequently in force.

This law has three main chapters: 1) First Chapter, that regulates the remission of interests and fines; 2) The Second Chapter contains incentives to attract private investment; and 3) Third Chapter contains several amendments to different legal bodies.

A. Incentives to attract investments

1. Income Tax Exemptions

a) For Prioritized Sectors

The Law of Productive Development stipulates that new productive investments initiated on or after the date of the enforcement of the law in the prioritized sectors, shall be entitled to the income tax exemption and the income tax advance during 12 years, counted from the first year that direct income only attributable to the new investment is generated. For those investments in the urban areas of Quito and Guayaquil, said exemption will be during 8 years.

In order for societies to benefit of this exemption, these shall generate net employment under the terms to be defined in the by-laws of the Law of Productive Development.

New productive investments in agro industrial, industrial and agro-associative prioritized sectors, within the cantons located in the boundaries, will benefit with a 15 years’ exemption.

Prioritized sectors are the following:

1. Agriculture sector: production of fresh, frozen and industrialized food.

2. Forestry and agroforestry chain and their processed products

3. Metal-mechanical

4. Petrochemical and oil-chemical

5. Tourism, film industry, audiovisuals and international events.

6. Renewable energies

7. Foreign commerce logistic services

8. Applied biotechnology and software

9. Exports of services

10. Software development and services, hardware production and development, digital infrastructure, computer security, digital products and contents, on-line services.

11. Energy efficiency

12. Industry of sustainable construction materials and technologies

13. Sectors of strategic replacement of imports and development of exports.

2. For Basic industries:

New productive investments that initiate on or from the date of the entering in force of the Law of Productive Development in the economic sectors determined as basic industries, shall be entitled to the income tax exemption during 15 years. The term of the exemption shall be counted from the first year with direct income only attributable to the new investment is generated.

In case those investments are made in cantons located at the borders, the tax exemption term will be of 20 years.

In order for societies to benefit of such exemption, these shall generate net employment, under the terms to be defined in the by-laws to the Law of Productive Development.

In this context, the following are considered basic industries:

1. Copper and aluminum smelting and refining

2. Steel smelting for the production of plain stainless steel.

3. Hydrocarbons refining

4. Petrochemical industry

5. Cellulose industry

6. Ships’ construction and repair

3. Exemption of the tax on the remittance of currencies

New productive investments for which an agreement had been entered into with the Ecuadorian government, for either sector of the economy, shall be entitled to the exemption of the tax on the remittance of currencies in their payments for:

a. Import of capital goods and raw materials for the development of the project, up to the amounts and in accordance with the terms that shall be defined in the investment contract.

b. Dividends distributed by local companies or foreign companies domiciled in Ecuador, in favor of effective beneficiaries that may be either individuals or corporations, during the terms stipulated in the investment contract.

For companies that reinvest in Ecuador at least 50% of its return, in productive assets, these will be exempt of the tax on remittance of currencies for payments abroad, for payment of dividends to effective beneficiaries residing in Ecuador.

B. Remission of Interests, Fines and Surcharges

a. Tax and Fiscal Obligations handled by the IRS

The Law of Producitve Development orders the remission of 100% of interests, fines and surcharges over the balance of tax obligations handled by the IRS. Such remission does not apply for tax obligations due after April 2, 2018, or for obligations derived from the annual income tax statement of fiscal year 2017.

In order to benefit from the remission, the taxpayers shall pay the total principal within the following deadlines:

1. Within 90 days after the publication of the Law of Productive Development, in case of (1) taxpayers with average gross income for the three latest fiscal years exceeding US$ 5 million; (2) individuals belonging to economic groups according to the IRS’ cadaster as of the date of enforcement of the Law; and (3) taxpayers holding obligations corresponding to withheld or perceived taxes.

2. The rest of taxpayers shall file applications requesting payment facilities or to pay the principal within 90 days from the entering into effect of the Law. Payment facilities for a term of up to 2 years can be granted.

b. Vehicle Registration and Transit violations

1. It is ordered the remission of interests on taxes on vehicles handled by the IRS and due as of April 2 2018, provided that the outstanding total shall be paid within 90 days from the date of entering in force of the Law.

2. It is ordered the remission of surcharges set forth by the National Transit Agency for lack of vehicle registration, due as of April 2 2018, provided that the total is paid within 90 days counted from the date of entering in force of the Law.

3. It ordered the remission of additional 2% fines under the Organic Transit Law, on transit violations, which payment is pending as of April 2 2018, provided that the total penalty is paid within 90 days from the date of entering in force of the Law.

c. Overdue Employers’ IESS obligations in law-suit

It is ordered the reduction of interests, fines and surcharges corresponding to obligations of employees’ affiliation at law-suit, arising from invoices or determination actions, glosses and credit titles issued by the IESS, as long as the payment is made within the following deadlines:

1. Payments within 90 days from the date of entering into effect of the Law may benefit of 99% of reduction of interests, fines and surcharges.

2. Payments made 91 to 150 days from the date of entering into effect of the Law may benefit of a 75% reduction of interests, fines and surcharges.

3. Payments made 151 to 180 days from the date of entering into effect of the Law may benefit of a 50% reduction of interests, fines and surcharges.

Such reduction is not applicable for obligations at law-suit for reserve funds, affiliation for non-remunerated work at home, collections, health extension, unsecured loans, collateral credits. Interests, fines and surcharges for the delayed affiliation filed after April 2, 218 are also excluded.

C. Amendment of several legal bodies

In addition, the Law to Promote Production includes important amendments to several legal bodies, among them:

a. Organic Law of the Internal Tax Regime

b. Law Amending the Law for the Tax Equity in Ecuador.

c. Organic Production, Commerce and Investments Code

d. Organic Monetary and Financial Code

e. Mining Law

f. Hydrocarbons Law

g. Labor Code

h. Social Security Law

i. Companies’ Act

In the next issue we will publish an analysis of the amendments that the Law to Promote Production will bring to general regulations.

JUVENILE WORK

Based on the activity, the minimum number of juvenile employees working at each company, with regards to the net increase in workers each fiscal year, is the following:

By ZVS Tobar in CORPORATE, M&A , INSURANCE , INSURANCE , News and Bulletins

The Ecuadorian Hydrocarbons Minister, along with other authorities of this field, visited Houston the first days of October to promote new projects and investment opportunities in the oil & gas sector. These projects and investment opportunities are both in the upstream and downstream sectors.

Positive news for investors seeking upstream projects, a sector that has been left almost exclusively to public investment, is the return to a participation sharing agreement, leaving behind the failed and most controversial service contract agreement that set a tariff per produced barrel of oil.

With the return to the participation sharing agreement under which the investor directly participates from the oilfield production, the Ecuadorian government sends a clear signal to the private investors seeking to improve oil production and stimulate the exploration of the South East of the Ecuadorian Amazon region.

These are the 4 investment projects in the agenda of the Ecuadorian government:

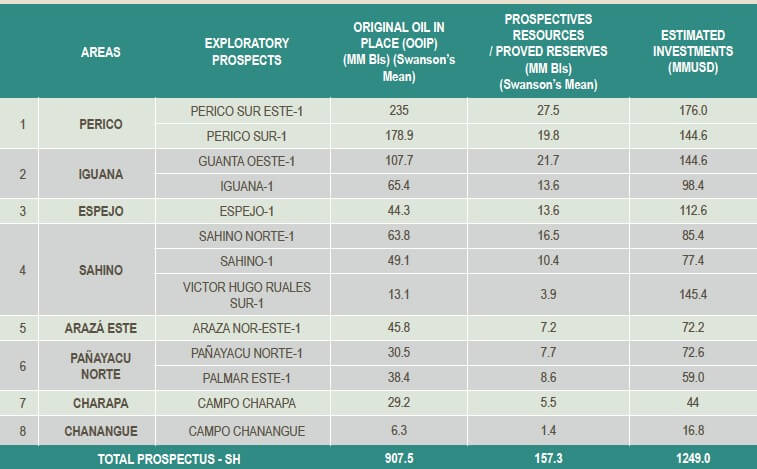

1. Intracampos Bid Round

The so-‐called “Intracampos” fields are composed by 8 blocks that include 13 fields, located in the Northeastern Ecuadorian Amazon region and are amongst oilfields in production. The total amount of proven reserves of the Intracampos oilfields is 157.3 MM bls of oil (907.5 MM bls of OOIP).

For the development of the Intracampos oilfields, the Ecuadorian government is expecting an approximate investment of USD 1.2 billion.

The Intracampos bidding round will probably be launched by the end of November or first days of December 2017.

2. South East Blocks

The South East of the Ecuadorian Amazon Region continues to be unexplored. Notwithstanding, it is an area that holds high expectations as there have been found 2 oil bearing reservoirs in Block 80 and the discovery in Block 64 of Peru (Situche Central) that is located in the border between Ecuador and Peru.

After the failed South East bidding round of 2013, under a service contract model by which the investor was paid with a tariff per produced barrel, this time the Government has made it clear that this new bid will be held under a participation sharing agreement, a model where investors are given an incentive as they can take advantage of any upside during the life of the contract.

This bidding is expected to be launched by the Ecuadorian government the first half of 2018.

3. Pacific Refinery

This was the flagship project of former President Rafael Correa´s administration, but it didn’t manage to attract investors due to the high amount of investment and unclear business model proposed.

This project’s justification is the limited refinery capacity of the country that is still unable to meet the internal fuel demand and, in turn, forces the government to make imports.

The Ecuadorian government has announced that this project requires an investment of USD 8.2 billion, almost half the sum announced by the prior government. Now the government expects private investment for the development of this project as it has stated that it would not compromise public funds.

The business model proposed for the development of this project has two options: (1) the payment by the Ecuadorian State of a tariff per refined barrel, which involves a BOT project; or, (2) the Ecuadorian State would sell the oil to the refiner at international price, and the Ecuadorian State would commit to buy the refined oil products from the refiner at international price.

Unlike the proposal by the former Government to refine oil imported from Venezuela, the current proposal is to refine the oil produced from the called ITT (Ishpingo-‐Tambococha-‐Tiputini) Blocks located in the Ecuadorian Amazon Region. Currently, the Tiputini oilfield produces 50,000 bpd, and the Government expects to increase its production to 100,000 bpd. The Ishpingo and Tambococha oilfields are expected to be developed in the short term.

The processing capacity of the Pacific Refinery has been proposed on 300,000 barrels per day.

4. Monteverde Maritime Project

The maritime terminal of Monteverde is an infrastructure in which the Government has already invested close to USD 600 million. The proposal is to find either a strategic partner to invest approximately USD 300 million for the development of a Regional Hub Storage and Distribution Center, or a private investor to buy this project to directly develop it.

This project finds attractive the fact that the Pacific Coast has a storage deficit for liquid products (fuel, chemicals) that, in turn, becomes an opportunity for the development of a Regional Hub Storage and Distribution Center. Moreover, taking into account the strategic position of Ecuador in the Pacific and the existence of infrastructure that needs to be improved and maximized.

The business model for this project has been left open to the investor needs, and can be developed under a concession model, a contract for the use of the infrastructure, a joint venture, or any other business model proposed by the investor.

By Tobar Bernardo in CORPORATE, M&A , Featured , News and Bulletins

This Doing Business in Ecuador Guide has been prepared by TOBAR ZVS C.L.1, and is intended to provide with general information for the knowledge of potential investors interested in acquiring an existing business or before starting operations in Ecuador.

The information included in this Guide is not exhaustive, and any in‐depth and detailed information shall be consulted with experts.

Read complete Doing Business in Ecuador Guide publication please Download

By ZVS Tobar in CORPORATE, M&A , News and Bulletins

This May one year ago the Ecuadorian Government notified those countries with which it had executed Bilateral Investment Treaties (“BITs’”), with the formal denunciation. As a consequence, those new foreign investments that are executed in Ecuador will no longer be subject, nor will they enjoy, the protection that the BITs’ granted to the nationals of the countries with a BIT. Therefore, we consider this to be an appropriate time to analyze in general terms the protection regime for foreign investment under Ecuadorian legislation.

As a general principle the Constitution recognizes and protects private property, which includes the investment made by private parties. The Constitution makes no exception to such principle that signifies that all private investment is protected under its terms, no matter its categorization (local, foreign, etc.).

Similarly, the Investment, Commerce and Production Code (“COPCI”) is in force since December 2010. The COPCI contains a detailed classification of the investment, differencing between: (1) investments for production, (2) new investments, (3) foreign investment, and, (4) local investment. The legal effect of this classification is important only to define which tax incentives apply to new investment and to the investment for production.

Moreover, the COPCI develops the constitutional principle that protects private property by recognizing other principles that naturally derive from the first. Non-discrimination is the first principle that the COPCI recognizes. Under this principle, all investors have the right to enjoy equal conditions for the administration, operation, expansion and transfer of their investments; additionally, foreign investors have the right to enjoy the same rights as local investors. The second principle recognized by the COPCI is the prohibition of arbitrariness. This principle provides that the investment cannot be subject to any arbitrary actions. The third recognized principle is an express prohibition on any form of confiscation[1].

In relation to the protection of foreign investments, and as was mentioned in the introduction, in May 2017 Ecuador denounced all the BITs’ that were in force with third nations. Most of the BITs’ contained provisions under which the protection granted was extended for an additional period of time[2] to those investments made until the effective termination date[3]. In that sense, foreign investments executed under the umbrella of a certain BIT and made before the BIT effective termination date, are protected and guaranteed by the terms of such treaty. On the other hand, new foreign investments to be made subsequently to the BIT’s effective termination date will no longer be protected by its terms.

As a consequence, the main instrument that a foreign investor currently has in order to protect its investment in Ecuador is an investment protection agreement with the Ecuadorian Government under the terms of the COPCI (an “Investment Protection Agreement”).

Under the COPCI and its regulations, any investor that (1) makes new investment[4], and (2) has a minimum disbursement of 250,000 USD during the first year, is eligible to request and sign an Investment Protection Agreement with the Government. The COPCI sets forth that under an Investment Protection Agreement the parties can establish: (a) the treatment that the Government shall grant to the investment, namely, the principles that shall govern and protect the investment and the rights granted to the investor; (b) stability over the tax benefits detailed in the COPCI; and, (c) national or international arbitration, provided that some conditions are met.

Since the entry into force of the COPCI, investors have used the Investment Protection Agreements mainly to obtain certain tax benefits and stability over their investments. They have developed a tax chapter in the agreement, leaving aside the investment protection chapter.

In this particular moment in which Ecuador has no longer valid BIT’s, and until the Ecuadorian Government signs the so called “Bilateral Investment Agreements” with third countries, the Investment Protection Agreements are the best instrument that a foreign investor has in order to agree to the principles that shall govern and protect the investment and the rights granted to the investor.

[1] There is one exception in the COPCI that allows for the confiscation of private property and relates to the expropriation of real state for the sole and only purpose of executing social development programs, sustainable projects for the environment and collective wellbeing. In the case of an expropriation for the detailed purposes, the Government must apply due process, prepare a valid assessment and pay the owner an adequate and fair compensation.

[2] Most TBIs’s provide for a protection period of 15 years counting from the effective termination date.

[3] The effective termination date for most of the TBI’s was 12 months from the date in which the Ecuadorian Government notified with the denunciation, which in most cases was done on May 16th, 2017.

[4] Under the COPCI new investment is defined as the flow of resources destined to increase the capital on the economy, through an effective investment in production assets that allow for (1) extend the future production capacity, (2) generate a larger level of production of goods or services, and (3) generate new employments.

By Sevilla Álvaro in CORPORATE, M&A , News and Bulletins